Smart Finance solutions for

your Business

Active user

15,000

download

49.9k

reviews

35.7k

partners

199+

LOAN AS PER REQUIREMENTS

FROM 7.50%

Offer Low Interest

48 HRS PROCESS

Fast & Easy Process

Shani Finserve Loan Magic Fast, Easy, Zero Drama in just 24-48 Hours

Need quick cash but don’t know how? At Shani Finserve, there are no queues, no confusion just smart and fast loans. We turn your dreams into reality.

- Click a button, not a hundred forms.

- Our team talks human, not bank-ish.

- Blink, and your docs are already verified.

- Before you panic your loan is approved.

- 1. Documents verifications is super easy here- we need basics

- 2. You can get loans super-fast here- without the drama.

Calculate Your Loan

& Get Detailed Insights

Plan your finances better with our advanced loan calculator that includes inflation adjustments and detailed payment schedules.

Finance Magic - Loans that Work for You

Welcome to Shani Finserve - where every money matter is handled easily, wisely, and without any stress. Whether you want to buy a car, chase a dream, or own your dream home, we can make it happen.

Here, we believe that money matters should not be scary, but simple and hassle-free. And if you're thinking about the future, we have you covered with our mutual fund and insurance solutions. So go ahead and dream big. We have your back.

Whatever You Need, We’ve Got a Loan

From professional growth to fulfilling your dreams, you need finance and for your financial needs- the name is Shani Finserve. With our wide range of loans, fast approvals, flexible terms, and expert support- we are here to make borrowing easier, smarter, and perfectly suited to your needs.

Personal Loan

For weddings, travel, emergencies or just because, a personal loan gives you both the money and the freedom to fund life on your terms. No collateral, quick approvals and flexible repayments make it the easiest way to turn "someday" into "right now."

Learn More

Business Loan

If you have a business dream but no finance to support it, this loan is for you. Whether you are expanding, hiring or just getting started, we offer funding that scales with your ambition. Minimal paperwork, maximum impact. Let your business do the talking.

Learn More

Loan Against Property

Got property? You can unlock its value and get a loan against it. With Shani Finserve, get high loan amounts at lower interest rates using your residential or commercial property as collateral. Perfect for big goals like education, business expansion or debt consolidation.

Learn More

Home Loan

Dream home? Get it now with easy EMIs and expert support every step of the way. Our home loan solutions are designed to help you own a house that is not just a dream but a plan. And this plan can start today!

Learn More

Vehicle Loan

Love that bike? Want that car? You can ride in style and class with a vehicle loan that gets you on the road even faster. No matter if it’s your first set of wheels or an upgrade, enjoy competitive rates, flexible terms and a smooth drive from application to approval.

Learn More

Education Loan

Turn your ambition into achievement with an education loan designed for students and their dreams. It covers tuition, travel and more, with flexible repayment options and quick disbursal because learning should never wait for funding.

Learn More

Used Car Loan

Get the car you love, minus the showroom price. Our used car loans offer fast approvals, attractive rates and up to 100% financing, making that pre-loved ride a very smart buy.

Learn More

Professional Loan

Doctors, CAs, architects - this one is for you. A professional loan gives qualified professionals the power to grow their practice, upgrade equipment or expand services with ease. Tailored financing for people who mean business.

Learn More

Equipment Loan

Machines that run your business shouldn’t slow it down. Our equipment loan helps you upgrade, replace or buy new assets without draining your capital. Quick funding, long-term benefits because the right tools matter.

Learn MoreShani Finserve Cooperates With These Banks

100+ Companies Trust Shani Finserve for Fast, Transparent, and Reliable Financial Services

Customer feedbacks

Best financial service provider in Dibrugarh. They also provide hassle-free and fast processing of all the services. Overall a great experience with Shani Finserve.

Rahul Das

Small Business OwnerShani Finserve is a blooming money market today. Great place to find all your financial needs under one roof. Thanks everyone 😊

Priyanka Deka

Marketing ExecutiveBest services for business loans, property loans & personal loans. They provide instant loan approval online in Assam.

Manoj Kalita

EntrepreneurAmazing service provided by the company—really smart and standard service. They are so systematic in all documentation work. Hats off to the team!

Neha Borthakur

HR ConsultantReally liked the way the team helps with loans. Must say, they are very responsive. Thank you 😊

Abhishek Sharma

FreelancerOur customer base

reaches India

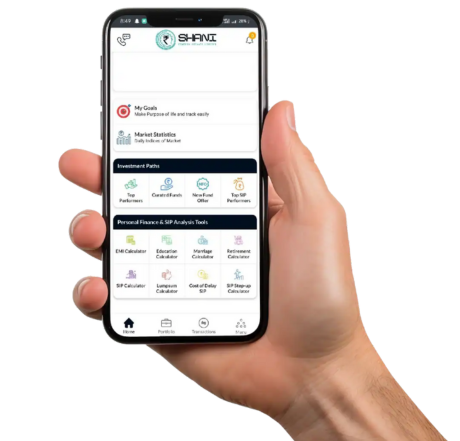

Get Started with Shani Finserve!

Experience seamless financial services right at your fingertips. Download our app today and take control of your financial journey.

Available on: